23 Aug 2017

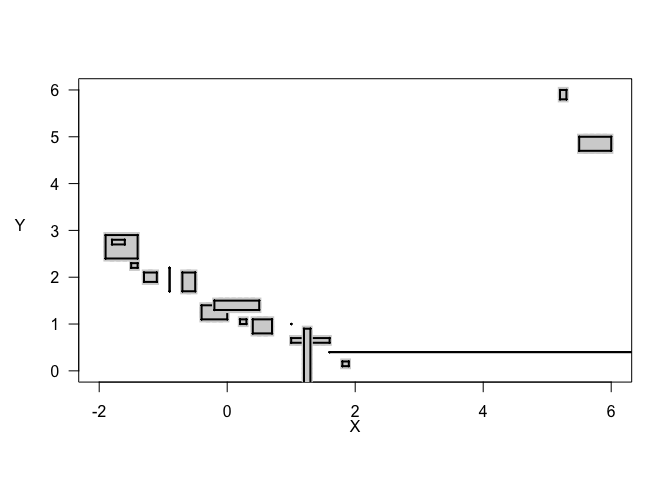

Imprecise regression is a generalization of linear regression that gives us stronger tools for modeling uncertainty. In a typical linear regression setting, we consider the input data to be precise observations: single points. In imprecise regression, we generalize the notion of observations to intervals rather than points. This allows us to more accurately represent scenarios with measurement error or other sources of uncertainty that make our input data “fuzzy”. This tutorial is based on the imprecise regression work in Cattaneo and Wiencierz (2012) and will teach you the fundamentals of this technique.

Imprecise regression is a generalization of linear regression that gives us stronger tools for modeling uncertainty. In a typical linear regression setting, we consider the input data to be precise observations: single points. In imprecise regression, we generalize the notion of observations to intervals rather than points. This allows us to more accurately represent scenarios with measurement error or other sources of uncertainty that make our input data “fuzzy”. This tutorial is based on the imprecise regression work in Cattaneo and Wiencierz (2012) and will teach you the fundamentals of this technique.

04 Aug 2017

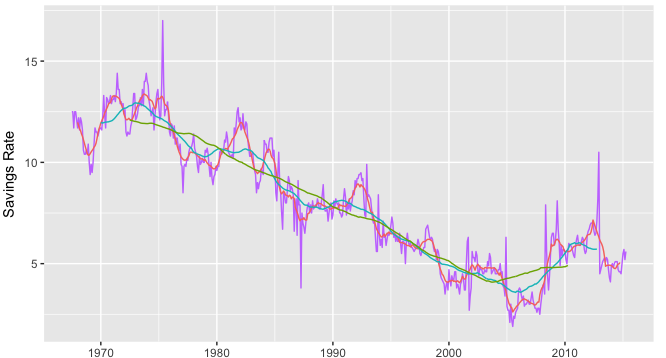

Smoothing methods are a family of forecasting approaches that average values over multiple periods in order to reduce the noise and uncover patterns in the data. Moving averages are one such smoothing method. In this new time series tutorial, you will learn the basics of performing smoothing averages.

Smoothing methods are a family of forecasting approaches that average values over multiple periods in order to reduce the noise and uncover patterns in the data. Moving averages are one such smoothing method. In this new time series tutorial, you will learn the basics of performing smoothing averages.

16 Jun 2017

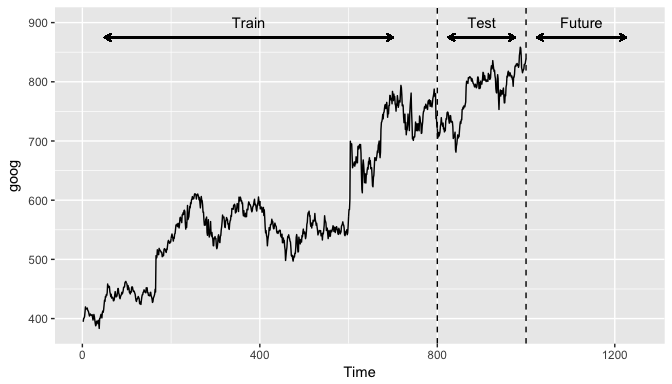

In this new time series tutorial, you will learn general tools that are useful for many different forecasting situations. It will describe some methods for benchmark forecasting, methods for checking whether a forecasting model has adequately utilized the available information, and methods for measuring forecast accuracy. These are important tools to have in your forecasting toolbox as each are leveraged repeatedly as you develop and explore a range of forecasting methods.

In this new time series tutorial, you will learn general tools that are useful for many different forecasting situations. It will describe some methods for benchmark forecasting, methods for checking whether a forecasting model has adequately utilized the available information, and methods for measuring forecast accuracy. These are important tools to have in your forecasting toolbox as each are leveraged repeatedly as you develop and explore a range of forecasting methods.

02 Jun 2017

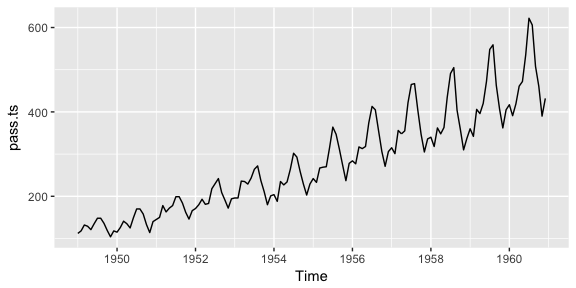

Time series forecasting is performed in nearly every organization that works with quantifiable data. Retail stores forecast sales. Energy companies forecast reserves, production, demand, and prices. Educational institutions forecast enrollment. Goverments forecast tax receipts and spending. International financial organizations forecast inflation and economic activity. The list is long but the point is short - forecasting is a fundamental analytic process in every organization. This new tutorial gets you started doing some fundamental time series exploration and visualization.

Time series forecasting is performed in nearly every organization that works with quantifiable data. Retail stores forecast sales. Energy companies forecast reserves, production, demand, and prices. Educational institutions forecast enrollment. Goverments forecast tax receipts and spending. International financial organizations forecast inflation and economic activity. The list is long but the point is short - forecasting is a fundamental analytic process in every organization. This new tutorial gets you started doing some fundamental time series exploration and visualization.

21 Apr 2017

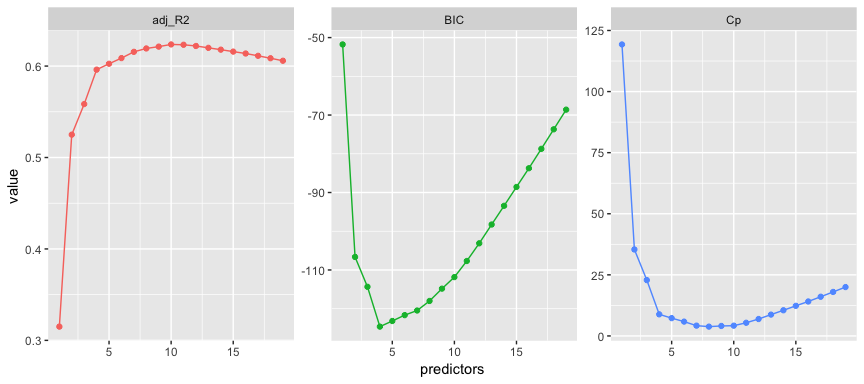

It is often the case that some or many of the variables used in a multiple regression model are in fact not associated with the response variable. Including such irrelevant variables leads to unnecessary complexity in the resulting model. Unfortunately, manually filtering through and comparing regression models can be tedious. Luckily, several approaches exist for automatically performing feature selection or variable selection — that is, for identifying those variables that result in superior regression results. This latest tutorial covers a traditional approach known as linear model selection.